What started as buzzword experimentation is quietly turning into market infrastructure. Here’s why that shift matters for the world’s fastest-growing economy.

For years, tokenization sat comfortably in the “interesting but distant” category – something worth watching, not acting on. That’s changed.

And Hong Kong is the clearest proof.

The city has moved from sandbox experiments to actual functioning products. In 2025, Hong Kong approved its first tokenized real estate investment structure, allowing fractional property ownership through blockchain-based systems. At the same time, the government issued a HK$10 billion (~$1.3 billion) tokenized green bond – demonstrating that large-scale financial instruments can already move on-chain. Through the Hong Kong Monetary Authority’s Project Ensemble, banks, asset managers and tokenized assets are now connecting inside a single live ecosystem.

“This is no longer a sandbox. It’s starting to look like a functioning market – and that changes the conversation entirely.”

Why real estate?

Real estate has always been one of the hardest assets to modernize. It’s large, illiquid and operationally complex – transactions take time, ownership structures are layered, and access is gated by capital. Tokenization doesn’t wave all that away, but it starts to restructure things. By enabling fractional ownership and digital representation of assets, property can begin to behave more like a financial product than a purely physical one. That’s the direction Hong Kong is clearly moving – and institutional players are already showing up.

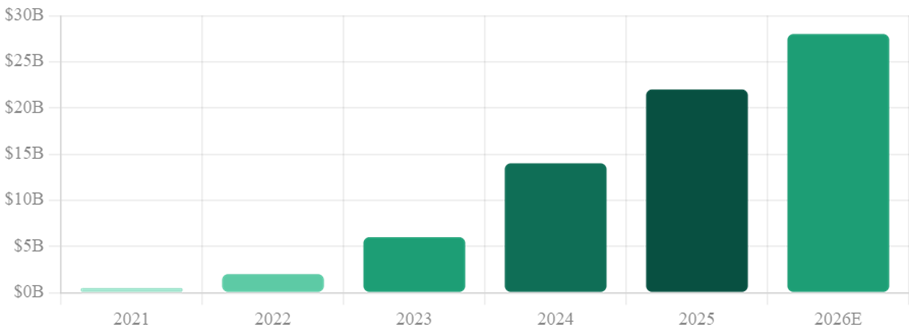

Global tokenized real-world asset growth (on-chain value, $B)

The numbers reinforce the momentum. Tokenized real-world assets have already crossed $25 billion in on-chain value and governments are now regularly issuing digital bonds. Institutions are testing tokenized funds. Secondary market infrastructure is being built. Hong Kong’s edge is in pulling all of this together at once – regulatory clarity, institutional participation, and live financial products in the same room.

What makes Hong Kong’s approach worth studying isn’t any single policy – it’s the combination.

Regulatory clarity tells institutions it’s safe to build. Institutional participation creates demand and legitimacy. Live financial products prove the model works outside a lab. Most jurisdictions have one or two of these; very few have all three working together. That’s the gap Hong Kong has quietly closed.

Tokenization readiness: Hong Kong vs India

Where India stands

India is still early in this story – and that’s not a criticism, it’s just the honest read. Platforms are being built, ideas are being tested, and the regulatory picture is still forming. But historically, financial innovation follows a clear arc: global hubs experiment first, institutions validate the model, and then other markets adapt it to their own context. Right now, we’re somewhere between the first and second stage. The window to shape how that adaptation happens in India is open – but it won’t stay that way forever.

The India signal

India’s real estate market is one of the largest in the world, yet fractional ownership remains structurally out of reach for most investors. Tokenization doesn’t just offer a tech upgrade – it offers a genuine rethink of access. What Hong Kong is proving is that this rethink can be done within a regulated, institutional framework. That’s the model worth watching.

The bigger picture

None of this is really about blockchain. It’s about what happens when assets that were once slow and illiquid get the infrastructure to behave differently. When regulation aligns with technology and institutions commit, the pace of change tends to surprise people. It doesn’t happen overnight – but once momentum builds, it accelerates fast. Hong Kong is at that inflection point now.

Tokenization doesn’t scale because the technology exists. It scales when markets allow it to function. Hong Kong is showing what that looks like. For India, the direction is already clear – the question is just how quickly it chooses to move.

With a strong interest in markets and emerging financial infrastructure, I’m driven by how thoughtful design and disciplined decision-making can create lasting value. My work centres on creating robust financial frameworks that balance innovation with stability and long-term impact. I believe the best outcomes come from patience, clarity and long-term thinking.

Connect: radhika@realx.in