For most of history, the world was full of valuable things.

Land – Infrastructure – Art – Private businesses everything was valuable.

But very few of these things were investable.

For centuries, wealth creation was concentrated in a relatively small set of financial instruments. Public equities, bonds and a limited number of real estate opportunities dominated investment portfolios. Everything else largely remained outside the financial system, owned directly by individuals, families, institutions or governments.

Today, that boundary is disappearing.

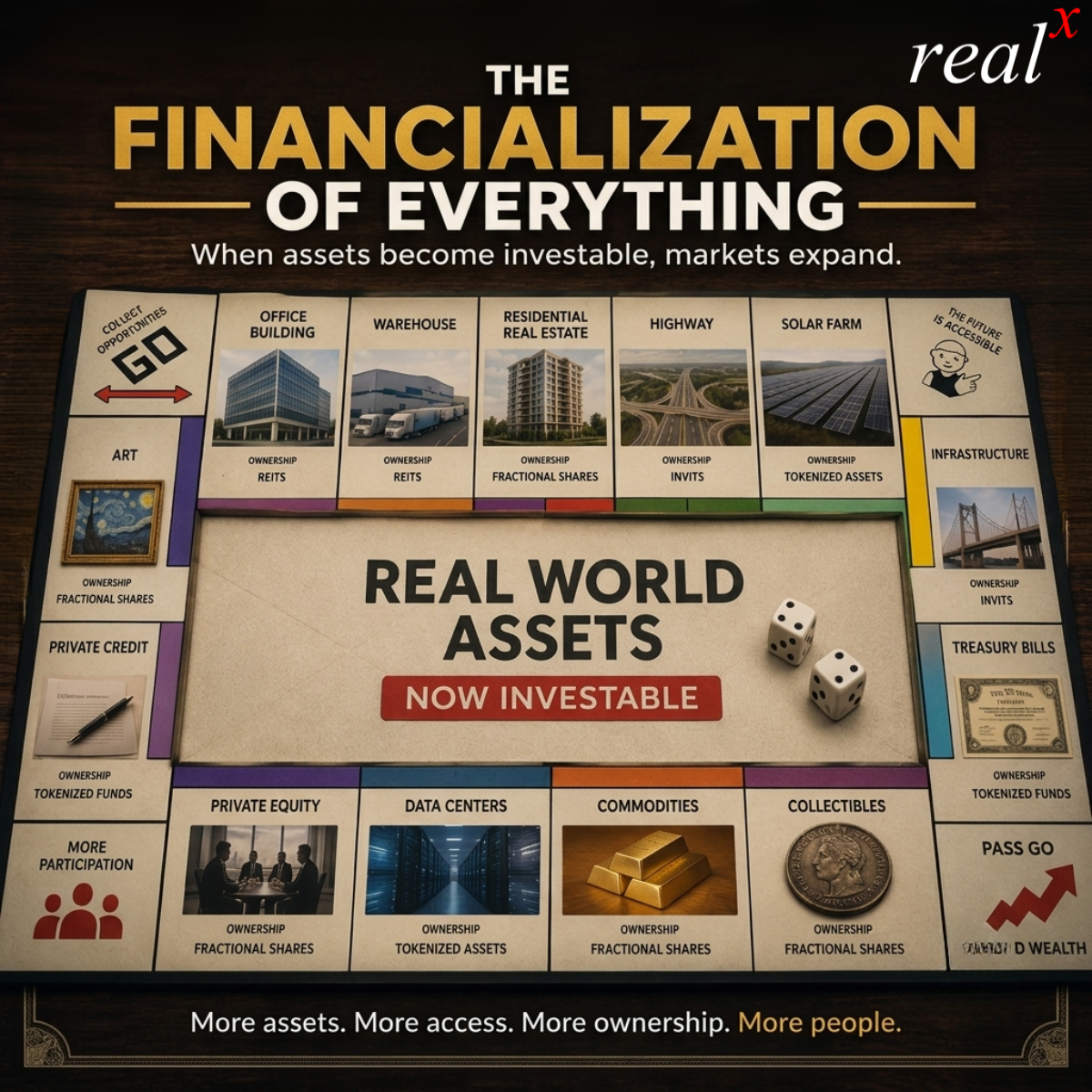

In the First Phase

Real estate became REITs.

Infrastructure became InvITs.

Government debt became ETFs and mutual funds.

Private credit is increasingly being packaged into investment vehicles.

Even traditionally illiquid assets such as artwork, collectibles and private market investments are being broken into smaller, investable units.The story of modern finance is no longer just about creating new assets. It is increasingly about making existing assets investable.

When Access Changes, Markets Change

| Era | Innovation | What Changed |

|---|---|---|

| 1600s | Public Markets | Ownership became investable |

| 1900s | Mutual Funds | Ownership became diversified |

| 1990s | ETFs | Ownership became simpler |

| 2000s | REITs / InvITs | Real assets became investable |

| 2020s | Fractional Ownership | Ownership became accessible |

| Emerging | Tokenization | Ownership becomes programmable |

One of the most powerful lessons in financial history is that markets tend to expand when access improves.

Consider exchange-traded funds (ETFs).

The underlying assets inside an ETF are not new. Investors have always been able to buy stocks and bonds individually. What ETFs changed was accessibility, diversification and ease of participation.

The result was extraordinary growth.

According to Citigroup, U.S. ETF assets under management reached approximately $10.4 trillion in 2025 and are projected to grow to $25 trillion by 2030. The growth is not being driven by new assets. It is being driven by better access to existing assets.

Real Estate and Infrastructure Offer a Case Study

India provides a useful example of this transformation.

For most investors, participating in large-scale commercial real estate or infrastructure project opportunities was inaccessible. That changed with the emergence of REITs and InvITs.

These structures transformed income-generating real estate and infrastructure assets into investment products that could be accessed through public markets.

The impact has been significant.

According to Knight Frank India, the combined assets under management of REITs and InvITs increased from approximately $42 billion in FY20 to nearly $94 billion in FY25. InvIT assets alone reached over $73 billion, while REIT assets crossed $20 billion.

The underlying roads, warehouses, office parks and infrastructure assets already existed.

What changed was participation.

Once access expanded, capital followed.

The Next Phase of Financialization

Participation in high-quality commercial real estate required significant capital and direct ownership. REITs lowered those barriers by allowing investors to access diversified portfolios through public markets. Fractional ownership took the concept further.

Instead of investing in a portfolio of assets, investors could gain exposure to specific properties with substantially lower capital requirements. Assets that were once accessible only to institutions or ultra-high-net-worth investors could now be owned by a broader pool of participants.

At its core, tokenization is simply the latest step in the financialization process. Just as ETFs transformed access to equities and REITs transformed access to commercial real estate, tokenization seeks to transform how ownership itself is recorded, transferred and distributed.

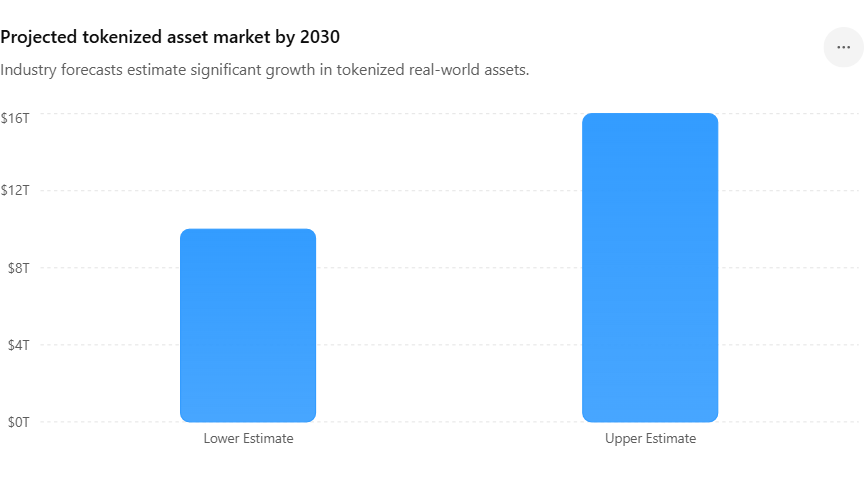

According to projections from multiple institutions including Boston Consulting Group and ADDX, the market for tokenized real-world assets could reach between $10 trillion and $16 trillion by 2030. Some forecasts suggest tokenized assets could account for a meaningful share of global financial assets within the next decade.

BlackRock’s tokenized treasury fund, BUIDL, surpassed $2 billion in assets under management within a year of launch. Franklin Templeton, JPMorgan, HSBC and several global financial institutions have launched or tested tokenized versions of traditional financial products. Regulators in jurisdictions such as Hong Kong, Singapore, the UAE and Switzerland are actively building frameworks for tokenized securities and real-world assets.

Taken together, these developments point toward a broader shift. The future of financialization is unlikely to be defined by entirely new asset classes.

Instead, it may be defined by new ownership infrastructure.

Throughout financial history, every major expansion in capital markets has been driven by improving access.

Tokenization has the potential to expand access even further by making ownership more divisible, transferable and globally accessible.

It is a story about ownership becoming accessible to more people than ever before.

With a strong interest in markets and emerging financial infrastructure, I’m driven by how thoughtful design and disciplined decision-making can create lasting value. My work centres on creating robust financial frameworks that balance innovation with stability and long-term impact. I believe the best outcomes come from patience, clarity and long-term thinking.

Connect: radhika@realx.in